“The average American family will see $2500 dollars per year in savings as a result of the ACA,” proclaimed the President as he campaigned for its passage. As much as he tried to hide the fact that the IRS would be the primary governmental body charged with enforcement of the ACA, he consistently touted his contention that insurance costs would go down. As we learn day by day, his claim was made without any basis in fact – another myth.

A myth only works as long as people believe it. And now, as more Americans, especially small businesses, experience not one, not two, but three annual double-digit rises in health insurance costs, the Administration and its supporters have suddenly stopped repeating the claim that rates would come down at all.

Instead, the Administration is now trying to spin this reality by saying the costs are going up less than they would have without Obamacare. So, their strategy is to switch the subject without much fanfare and hope the voters don’t notice. That strategy worked in the 2012 Election and will continue to succeed so long as the GOP keeps failing to bring this to the fore in a way that most Americans can understand.

In the face of this inconvenient truth, the Administration adroitly changed the terms of the debate and claimed victory over the hypothetical “even higher rates” that would have occurred had it not been for Obamacare. They were not challenged by the press, nor their political opponents, so score one for Mr. Obama.

A good example of how the Administration is finding success with disingenuous arguments is when they make a tomatoes to potatoes comparison by detailing younger Americans’ health care costs pre and post-Obamacare implementation. They say that younger Americans will pay about the same rate for individual policies as it costs for the group policies now provided by their employers. Nice try; employer-covered plans and individual plans are rarely equivalent and the latter are about to go up dramatically more so than the former.

Moreover, it is a reasonable assumption that younger people especially will be purchasing their own individual plans as employers find it a poor business decision to maintain their employer-sponsored plans. The major reason for this will likely be the fact that small businesses are about to pay higher taxes to help support the State exchanges. Those taxes are helping to subsidize the very State Exchanges, which are designed to help workers qualify for a government subsidy and find health insurance at lower rates. So why would an employer want to pay the inflated insurance costs (plus the aforementioned higher taxes) to cover his employees while also footing the bill for the state exchange leaving the employee unable to capture the subsidy available to them? In fact, it is expected that millions will lose their employer-sponsored plans over the next 5-6 years.

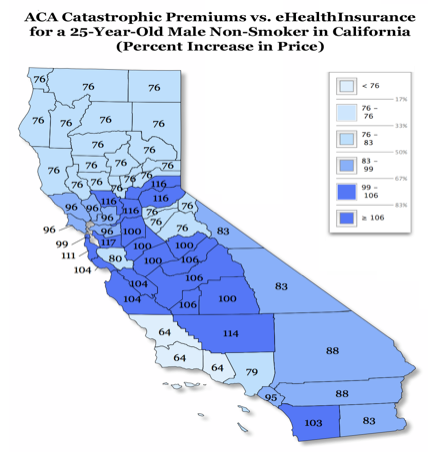

So, what do we expect as these employees look to the exchanges for their health care? The graphic below, taken from a wonderfully informative article by Manhattan Institute’s Avik Roy, shows just how much of a boost in rates are expected for California’s average healthy younger Californian.

There was never going to be lower health insurance costs under Obamacare and any clear-eyed perusal of the law makes that obvious. Why the President promised otherwise we may never know. But if you force health insurers to provide more services to more people then take away any ability to install an appropriate risk rating system focring them to provide services on demand and with no-copayments, then higher fees are guaranteed. The result – fees are going up, not down….and in a big way.