But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? – Alan Greenspan

California has struggled the past six years to recover from the Great Recession. But recent economic statistics suggest that the Golden State is finally regaining its luster.

A few examples:

- The Economic Development Department (EDD) reports that California added 39,800 nonfarm payroll jobs in March, dropping the state’s unemployment rate to 6.5 percent. The unemployment rate is down from 6.7 percent the previous month and 7.9 percent a year ago.

- The Legislative Analyst’s Office (LAO) shows that April’s personal income tax collections so far have exceeded the Governor’s projections by $750 million. Current collections are up 24 percent over a comparable period last year.

- And the Public Policy Institute of California (PPIC) indicates that since December 2014, at least 50 percent of adults in the state believe that we will have good times financially during the next twelve months. The last time this figure reached the 50 percent level was January 2007.

This is all very good news for California. And many – myself included – also would chime in to say that it’s about time.

But some in Sacramento are mistaking this good data as a sign that the state’s economy is now completely healed. And as a result they are proposing new, landmark legislation that promises to impose significant costs onto Californians.

Notably, Senate Bill 8 (the Upward Mobility Act) would levy sales taxes on most services across the state – everything from accounting to car repair to hair styling. The goal is to generate at least $10 billion more in tax revenue for state and local governments. Another bill, Senate Bill 350 (the Clean Energy and Pollution Reduction Act of 2015), would increase the cost of electricity for businesses and residences by requiring that the state obtain 50 percent of its electricity from renewable (and expensive) sources such as solar power and wind. The bill further mandates that California reduce its gasoline usage for transportation by 50 percent, and increase the energy efficiency of existing buildings by 50 percent.

Now is not the time for Sacramento to place additional burdens on households and businesses. That’s because, despite the recent good news, California’s economy is still recovering.

How do we know we’re not back to normal? One indication comes from Harvard professors Carmen Reinhart and Kenneth Rogoff. Reinhart and Rogoff examined 100 systemic banking crises – like the financial crisis we just experienced – and found that on average it takes about eight years for countries to reach their pre-crisis level of income (as measured by real per capita GDP). Although the United States took about five to six years to recover from the Great Depression by this measure, recall that California experienced a relatively deeper shock (as measured by unemployment) and lagged the United States in its recovery.

But we also know this from digging deeper into the data. Consider the three examples that I mentioned earlier:

- While EDD reported that the state’s unemployment rate is now 6.5 percent, this unemployment rate is associated with a very low labor participation rate of 62.3 percent. Prior to the Great Recession, this level had not been seen since 1976. If California’s current labor participation rate matched the 65.3 percent that we saw as the Great Recession ended in June 2009, another 2.1 million Californians would be unemployed today and the state’s unemployment rate would stand at 10.8 percent.

- Although personal income tax collections have exceeded expectations this year, the personal income tax is an unreliable indicator of the strength of California’s economy. As government watchers know, the state relies heavily on the personal income tax and it has become increasingly volatile.

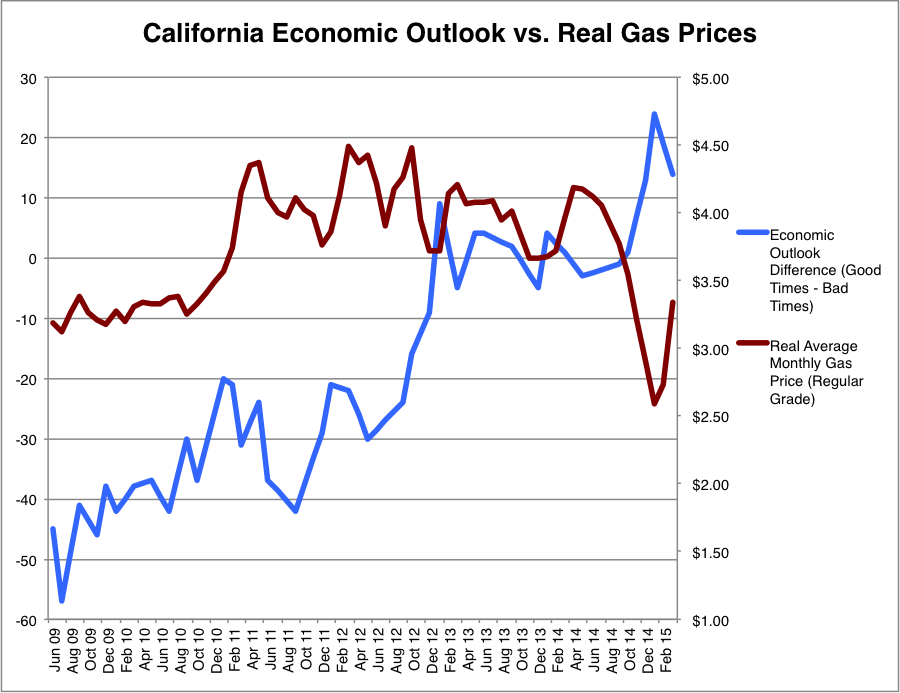

- And while the economic outlook of Californians has hit new highs of late, one could argue that this uptick actually has more to do with the fall in the price of gasoline than any other factor. The figure below compares PPIC’s economic outlook (shown as the difference between those expecting good times ahead and those expecting bad times) against California’s monthly average gas prices for regular gas, provided by the California Energy Commission and adjusted by me for inflation, from the end of the Great Recession. The figure shows the economic outlook generally trending upwards over time as the economy rebounds, but noticeably spiking upwards as gas prices fell to near $2.50 in the latter half of 2014.

So the California economy has not yet healed. But in its (irrational) exuberance over the current condition of the economy, Sacramento is promoting legislation that threatens the recovery. As a result we risk creating “unexpected and prolonged contractions” of our own.

So the California economy has not yet healed. But in its (irrational) exuberance over the current condition of the economy, Sacramento is promoting legislation that threatens the recovery. As a result we risk creating “unexpected and prolonged contractions” of our own.

This reminds me (of all things) of my neighbors’ recently reconstructed driveway. The contractors advised them to keep off it completely for two weeks while it cured – if they left it alone it would last them for decades, but if they didn’t they could do lasting damage.

At some point, Californians should have an open and honest discussion about the future of the state’s tax policy, energy policy and other major initiative. But for now, it makes sense to keep off the economy while it cures. We’ll be happy that we did.

Dr. Justin L. Adams is the President and Chief Economist of Encina Advisors, LLC, a Davis-based research and analysis firm.