Cross Posted on NewGeography.com

For some time, theorists have been suggesting that it is time to

redefine the American Dream of home ownership. Households, we are told,

should live in smaller houses, in more crowded neighborhoods and more

should rent. This thinking has been heightened by the mortgage crisis

in some parts of the country, particularly in areas where prices rose

most extravagantly in the past decade. And to be sure, many of the

irrational attempts – many of them government sponsored – to expand

ownership to those not financially prepared to bear the costs need to

curbed.

But now the anti-homeowner interests have expanded beyond reigning

in dodgy practices and expanded into an argument essentially against

the very idea of widespread dispersion of property ownership. Social

theorist Richard Florida recently took on this argument, in a Wall Street Journal article entitled "Home Ownership is Overvalued."

In particular, he notes that:

The cities and regions with the lowest levels of homeownership-in the

range of 55% to 60% like L.A., N.Y., San Francisco and Boulder-had

healthier economies and higher incomes. They also had more highly

skilled and professional work forces, more high-tech industry, and

according to Gallup surveys, higher levels of happiness and well-being.

(Note)

Florida expresses concern that today’s economy requires a more

mobile work force and is worried that people may be unable to sell

their houses to move to where jobs can be found. Those who would reduce

home ownership to ensure mobility need lose little sleep.

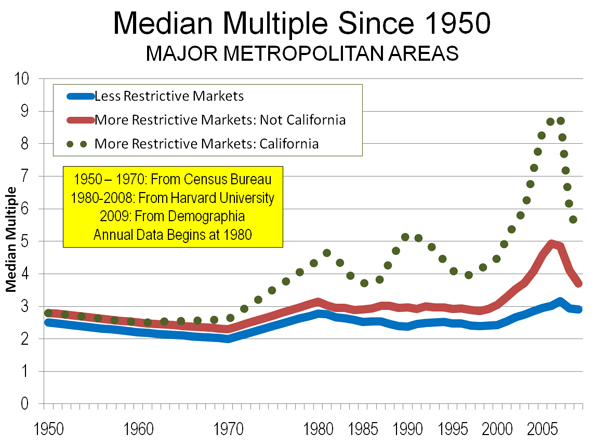

The Relationship Between Household Incomes and House Prices

It is true, as Florida indicates, that house prices are generally

higher where household incomes are higher. But, all things being equal,

there are limits to that relationship, as a comparison of median house

prices to median house prices (the Median Multiple) indicates. From

1950 to 1970 the Median Multiple averaged three times median household

incomes in the nation’s largest metropolitan areas. In the 1950, 1960

and 1970 censuses, the most unaffordable major metropolitan areas

reached no higher than a multiple of 3.6 (Figure).

This changed, however, in some areas after 1970, spurred by higher Median Multiples occuring in California.

William Fischel

of Dartmouth has shown how the implementation of land use controls in

California metropolitan areas coincided with the rise of house prices

beyond historic national levels. The more restrictive land use

regulations rationed land for development, placed substantial fees on

new housing, lengthened the time required for project approval and made

the approval process more expensive. At the same time, smaller

developers and house builders were forced out of the market. All of

these factors (generally associated with "smart growth") propelled

housing costs higher in California and in the areas that subsequently

adopted more restrictive regulations (see summary of economic research).

During the bubble years, house prices rose far more strongly

in the more highly regulated metropolitan areas than in those with more

traditional land use regulation. Ironically many of the more regulated

regions experienced both slower job and income growth compared to more

liberally regulated areas, notably in the Midwest, the southeast, and

Texas.

Home Ownership and Metropolitan Economies

The major metropolitan areas Florida uses to demonstrate a

relationship between higher house prices and "healthier economies" are,

in fact, reflective of the opposite. Between August 2001 and August

2008 (chosen as the last month before 911 and the last month before the

Lehman Brothers collapse), Bureau of Labor Statistics data indicates that in the New York and Los Angeles metropolitan areas, the net job creation rate trailed

the national average by one percent. The San Francisco area did even

worse, trailing the national net job creation rate by 6 percent, and losing jobs faster than Rust Belt Pittsburgh, St. Louis, and Milwaukee.

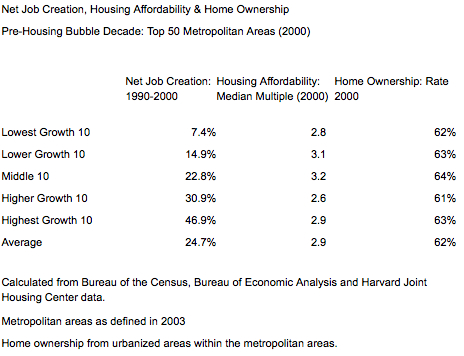

Further, pre-housing bubble Bureau of Economic Analysis

data from the 1990s suggests little or no relationship between stronger

economies and housing affordability as measured by net job creation.

The bottom 10 out of the 50 largest metropolitan areas had slightly

less than average home ownership (this bottom 10 included "healthy" New

York and Los Angeles). The highest growth 10 had slightly above average

home ownership (measured by net job creation). Incidentally, "healthy"

San Francisco also experienced below average net job creation, ranking

in the fourth 10.

Moreover, housing affordability varied little across the categories of economic growth (Table).

Home Ownership and Happiness

If Gallup Polls on happiness were reliable, it would be expected

that the metropolitan areas with happier people would be attracting

people from elsewhere. In fact, people are fleeing with a vengeance. During this decade alone, approximately one in every 10 residents have left for other areas.

- The New York metropolitan area lost nearly 2,000,000 domestic

migrants (people who moved out of the metropolitan area to other parts

of the nation). This is nearly as many people as live in the city of Paris. - The Los Angeles metropolitan area has lost a net 1.35 million

domestic migrants. This is more people than live in the city of Dallas. - The San Francisco metropolitan area lost 350,000 domestic

migrants. Overall, the Bay Area (including San Jose) lost 650,000, more

people than live in the cities of Portland or Seattle.

Why have all of these happy people left these "healthy economies?"

One reason may be that so many middle income people find home ownership

unattainable is due to the house prices that rose so much during the

bubble and still remain well above the historic Median Multiple. People have been moving away from the more costly metropolitan areas. Between 2000 and 2007:

- 2.6 million net domestic migrants left the major metropolitan areas

(over 1,000,000 population) with higher housing costs (Median Multiple

over 4.0). - 1.1 net domestic migrants moved to the major metropolitan areas with lower house prices (Median Multiple of 4.0 or below).

- 1.6 million domestic migrants moved to small metropolitan

areas and non-metropolitan areas (where house prices are generally

lower).

An Immobile Society?

Florida’s perceived immobility of metropolitan residents is curious.

Home ownership was not a material barrier to moving when tens of

millions of households moved from the Frost Belt to the Sun Belt in the

last half of the 20th century. During the 2000s, as shown above,

millions of people moved to more affordable areas, at least in part to

afford their own homes.

Under normal circumstances (which will return), virtually any

well-kept house can be sold in a reasonable period of time. More than

750,000 realtors stand ready to assist in that regard.

Of course, one of the enduring legacies of the bubble is that many

households owe more on their houses than they are worth ("under

water"). This situation, fully the result of "drunken sailor" lending policies, is most severe in the overly regulated housing markets in which prices were driven up the most. Federal Reserve Bank of New York

research indicates that the extent of home owners "under water" is far

greater in the metropolitan markets that are more highly restricted

(such as San Diego and Miami) and is generally modest where there is

more traditional regulation, such as Charlotte and Dallas (the

exception is Detroit, caught up in a virtual local recession, and where

housing prices never rose above historic norms, even in the height of

the housing bubble). Doubtless many of these home owners will find it

difficult to move to other areas and buy homes, especially where

excessive land use regulations drove prices to astronomical levels.

Restoring the Dream

There is no need to convince people that they should settle for less

in the future, or that the American Dream should be redefined downward.

Housing affordability has remained generally within historic norms in

places that still welcome growth and foster aspiration, like Atlanta,

Dallas-Fort Worth, Houston, Indianapolis, Kansas City, Columbus and

elsewhere for the last 60 years, including every year of the housing

bubble. Rather than taking away the dream, it would be more appropriate

to roll back the regulations that are diluting the purchasing power and

which promise a less livable and less affluent future for altogether

too many households.

—

Note. Among these examples, New York is the largest metropolitan

area in the nation. Los Angeles ranks number 2 and San Francisco ranks

number 13. The inclusion of Boulder, ranked 151st in 2009 seems a bit

curious, not only because of its small size, but also because its

advantage of being home to the main campus of the University of

Colorado. Smaller metropolitan areas that host their principal state

university campuses (such as Boulder, Eugene, Madison or

Champaign-Urbana) will generally do well economically.

Photograph: New house currently priced at $138,990 in suburban Indianapolis (4 bedroom, 2,760 square feet). From http://www.newhomesource.com/homedetail/market-112/planid-823343